The Future of HCM in the SMB

Where is the market headed?

Technology has completely changed the game for HCM in the small to midsize employer market, which The Starr Conspiracy Intelligence Unit defines as companies with fewer than 2,500 employees. Software-as-a-Service technology, enabled by wide availability of high-speed Internet connections and mobile devices, now allows small and midsize businesses (SMBs) the ability to automate, outsource, manage, and accelerate business processes in a way that was formerly the exclusive domain of large enterprises, especially when it comes to people processes. Even though businesses have been able to outsource payroll for decades, SMBs today have the ability to deploy entire platforms for payroll, benefits, compliance, talent, and analytics.

The market opportunity in the United States alone is huge. SMB companies comprise 60 percent of the U.S. workforce, account for $2.95 trillion in annual payroll, and include 56 million small-business employees and 13.9 million midmarket employees. By comparison, enterprise companies (2,500 or more employees) have 46.5 million employees and $2.2 trillion in annual payroll. In terms of opportunity, you would probably be surprised with how unsophisticated some of the companies in this segment are. You would think that a 2,000-employee company would have a high level of process and technology capability. After all, with a conservative assumption of $100,000 in annual revenue per employee, you are talking about a $200 million company. However, many companies of this size still rely on paper-based and manual processes.

Along the way, the lines between subcategories of HCM have blurred. Stand-alone point solutions such as payroll and benefits administration will continue to exist, and many buyers will continue to purchase these solutions individually. However, companies that deliver only point solutions are vulnerable to disintermediation. Payroll is a perfect example — ADP, Ceridian, and Ultimate Software have built out platforms to serve the full employee life cycle. SAP has built out a full global payroll capability in a short period of time. Even upstarts such as Gusto (formerly ZenPayroll) are expanding into other areas, such as benefits. These moves are as much defensive as they are focused on growth.

As a result, we are seeing companies we wouldn’t typically consider category competitors starting to compete with each other. TriNet is a PEO, right? Yes. But we also see them as an HCM company. Are Zenefits and Workday competitors? Not yet, but they could both be competing for customers in the upper midmarket (1,000- to 2,500-employee companies), though we believe they would be going after very different buyers.

For most of the SMB HCM space, the buyers are about getting stuff done, not getting the proverbial “seat at the table.” We see many small companies as simply wanting to make HR something they don’t need to worry about. In the midmarket, we see companies, even as small as a few hundred employees, that are growing and competing more strategically with larger companies across industry segments. As they do this, they’re thinking about their workforce more strategically. They’re also looking for a better user experience that’s in line with other tools they have long used in their businesses (finance, marketing, etc.) and their consumer experiences such as Facebook and Google. We’ve heard this from professional service firms, tech firms, and even construction equipment manufacturers.

We also see the market as a whole less concerned with platforms and more concerned with using tools that will scale with their business’s growth and connect easily as new solutions are added. It’s point solutions that can integrate — and platforms that can integrate. The platforms in the market today — ADP especially — have a legacy of difficulty here.

As a result, TSCIU sees seven major trends shaping the SMB HCM market:

- The rise of compliance as service. HR has always been in the business of compliance as its primary job. However, the passage and survival of the Affordable Care Act have escalated the degree of difficulty in compliance exponentially. The stakes are high, and the process is confusing. Many SMB HCM vendors will benefit as companies scramble to comply.

- The evolution of the group health plan. A sea change is underway in how employees get benefits coverage. This is the change that no one is talking about — yet.

- The disintermediation of the benefits broker model. In a hardball category, expect the roughest fight to be here.

- The growing contingent workforce. As more employees work on something other than a full-time basis, expect tectonic shifts in the workforce everywhere.

- Security is looming as an issue. HCM is where the concentration of employees’ personal data is. It’s not a matter of if it’s a target, but how bad can it get.

- Rebalancing the scales between technology and services. Buyers want a greater level of service than most SaaS business models will allow. So now what?

- Blending of communication tools and functional tools. Buyers’ expectations about HR technology are facing a dramatic shift.

So what do all of these trends mean?

For HCM vendors, there are many roads to the future. Are you a market-share player battling for dominance? Or are you a profit-focused company and acquisition target? You should know who you are and be that. You must also expand your idea of what a competitor looks like. You may find yourself battling a competitor in a year or two that isn’t even in your category today. What’s your vision for the future and your strategy for getting there? If you don’t know, you’re already behind.

For HCM buyers, ask more questions about ongoing customer success. How is your provider going to support you after implementation? Also, understand your exit strategy. The solution you choose today may not fit so well in a year or two. Avoid vendor lock as much as possible.

For HCM investors, pick your portfolio carefully. There are a lot of good companies in this market, but the best idea and the best technology don’t always win. We believe this is a very dangerous market from an investment standpoint. Category leaders will fall and promising upstarts will flame out. Be careful about using brand power as a proxy for due diligence. This is a market that values experience and risk mitigation. Look at the leadership and how they approach the market. It will be telling about odds for success.

Market Stage

Generally speaking, we at TSCIU find the word “disruption” to be incredibly misused. It’s a lot like “employee engagement” — it carries a ton of gravitas, yet it’s also fluffy and meaningless. People use the term “disruptive” when they mean “innovative” or even “sort of an interesting idea.” And don’t even get us started on “unicorns.” We believe that entrepreneurs and investors focus on the far more humble and useful goals, like building good companies that deliver high-quality products and services that solve real business problems.

There’s a far more disturbing similarity that “disruption” and “employee engagement” share. These terms don’t indicate outcomes; these terms indicate the catalyst. Employee engagement allows companies to experience many positive business outcomes — higher revenue and profit per employee, greater innovation, faster growth, lower turnover, reduced healthcare costs, and so on. Disruption is merely the catalyst that changes a market, resets the vision of what customers want and companies pursue, and puts revenue and market share in play.

To use the term far more properly, HCM today is a perfect example of what a disrupted market looks like. Overall, the market would seem to be a mature one. Some of the world’s biggest and best-known brands inhabit the space — including ADP, Oracle, and SAP. However, given that we see barely one-fifth of the addressable market penetrated and many brands with new and different approaches — including Workday, Ultimate Software, TriNet, and Zenefits — we believe this market is just now entering its early mainstream phase.

Market Size

In the course of our research about the SMB market, we discovered that the size of the SMB HCM market, as well as the overall HCM, was far larger that even we first thought. The Starr Conspiracy Intelligence Unit estimates that the total addressable market (TAM) for SMB HCM is huge — $95.3 billion. Although HRIS and talent management grab most of the headlines, we see the biggest opportunities is in core HR — benefits ($33.5 billion), compliance ($20.9 billion), and payroll ($26.8 billion). Furthermore, we believe that the SMB is larger than the enterprise market by $12.2 billion. We also believe that the TAM for HCM is $178.4 billion — far larger than the $131 billion figure when we assessed the TAM earlier in 2015.

To be clear, when we are talking about benefits, we are talking about outsourced benefits administration and management, not the actual benefits themselves. Health benefits alone typically make up about 8 percent of payroll, which means that SMB companies are paying $200 billion for the actual health benefits themselves.

So why is the size of the market so large? We believe that market projections for payroll and benefits services, PEO, BPO, talent management, talent acquisition, and HR services must also be considered. These companies are more than just Software-as-a-Service. We see more and more service being expected and demanded by the market, and as a result, delivered by more vendors.

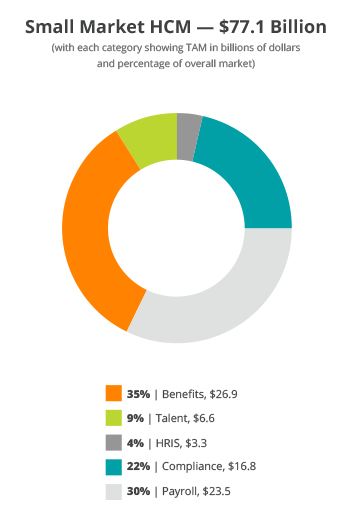

As we begin to break down the SMB market further, the size of the opportunity in small market HCM (fewer than 500 employees) begins to stand out dramatically from midmarket companies (with between 500 and 2,500 employees).

A breakdown of the small business HCM technology market by company size and solution subcategories reveals an almost symmetrical breakdown between sub-20-, 20- to 99-, and 100- to 499-employees companies. It’s easy to see how each of these has been broken down as separate HR industries — PEO, HRO/ASO, and HCM. It’s also easy to see why core HR is becoming the battleground in this market segment. Companies are going where the money is.

Although smaller by revenue opportunity, the midmarket has become a very competitive market. You’re getting smaller HCM companies moving up-market and enterprise players going down-market. An $18.1 billion opportunity is hard to pass up.

Market Share

When it comes to market share, ADP is dominant, with almost one-third of the market. The next-closest competitors — TriNet and Paychex — are 20 percentage points behind. Based on our market overview, we see the dominance of these two companies in the sub-100-employee segment as the reason.

If you factor out ADP and evaluate market share, two interesting things occur. First, Ceridian moves into the category leader ranks, and with its Dayforce platform, we see it well positioned to challenge in the category with lots of midmarket growth. Second, Zenefits — the best-known upstart brand in SMB HCM — clocks in with 2 percent. It’s a clear indication of how volatile this market is. There will be dramatic swings in market share to come. There’s too much market available, too much money flowing into the market, and too little barrier for switching to prevent volatility and disruption.

Market Growth

It’s early days for this market. We see only 10 percent SMB market penetration. However, expect growth to be fast — CAGR of 8 to 12 percent. Market leaders will grow 50 to 200 percent year over year. We believe the benefits component is the fuel for growth. We saw Zenefits do it, and we are seeing other smaller players experience 100 percent or better growth as well.